How I Rebuilt My Finances During a Debt Crisis — What Really Worked

I used to lie awake at night staring at my bills, feeling trapped by debt I didn’t know how to fix. It wasn’t just stress — it was survival. I tried quick fixes that made things worse. But eventually, I found a smarter way: not just cutting costs, but rebuilding my investment layout from the ground up. This isn’t theory — it’s what actually pulled me out. If you're drowning, this might be the lifeline you need.

Hitting Rock Bottom: When Debt Feels Like a Trap

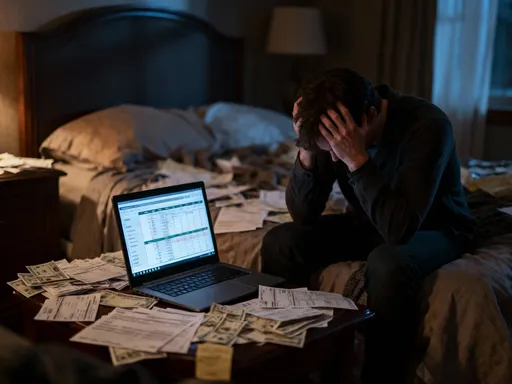

There was a time when opening the mailbox felt like facing a courtroom. Every envelope carried a verdict: late fees, final notices, interest hikes. My income hadn’t changed much, but life had — medical expenses for a family member, a car repair that came out of nowhere, and months of reduced work hours due to seasonal shifts. What started as manageable credit card balances snowballed into something far more dangerous. Minimum payments barely dented the principal, and new charges crept in just to cover groceries and utilities. The numbers on the statements grew faster than my ability to respond.

What made it worse was the isolation. I didn’t talk about it — not with friends, not with family. There was shame in admitting I couldn’t keep up, even though I worked hard and had always believed I was responsible. Budgeting apps helped a little, but they couldn’t stop the tide. I cut back on dining out, canceled subscriptions, and shopped exclusively at discount stores. Still, the debt climbed. That’s when I realized something crucial: cost-cutting alone wasn’t enough. When your liabilities exceed your liquid assets, and your cash flow is stretched thin, traditional advice falls short. I needed a different kind of strategy — one that didn’t just slow the bleeding, but healed the wound.

The turning point came when I stopped seeing my situation as a personal failure and started viewing it as a systems failure. My financial structure had no resilience. There was no emergency buffer, no diversified income, and no long-term investment plan — only reactive spending and mounting obligations. I had treated money as something to be managed day-to-day, not designed for stability. This realization didn’t bring relief, but it did bring clarity. If the system was broken, I needed to rebuild it — not patch it.

Shifting the Mindset: From Survival to Strategy

Recovery began not with a spreadsheet, but with a shift in thinking. For months, I operated in survival mode — making minimum payments, avoiding calls, hoping something would change. But hope isn’t a plan, and fear-driven decisions rarely lead to progress. I started reading about personal finance not for quick tips, but for principles. I learned that financial health isn’t just about how much you earn or save, but how your money is structured. That’s when I encountered the concept of investment layout — not as a tool for wealth building only, but as a framework for financial resilience.

Investment layout, in this context, doesn’t mean chasing stocks or crypto. It means designing how your money flows — where it’s allocated, how it’s protected, and how it grows over time. It’s the architecture behind your financial life. I had never thought of myself as someone who needed an investment strategy while in debt. But the truth is, everyone does. Even if you’re paying off balances, the way you manage your remaining cash, your savings habits, and your risk exposure shapes your recovery path. Without a layout, you’re just reacting. With one, you’re steering.

This mindset shift changed everything. Instead of asking, “How can I make this payment?” I began asking, “How can I restructure my finances so this doesn’t happen again?” That question led me to prioritize long-term stability over short-term fixes. I stopped looking for loopholes and started building foundations. I accepted that progress would be slow, but I also understood that slow progress, when consistent, compounds just like interest — only in the right direction. The emotional weight didn’t disappear overnight, but it became manageable because I had a plan, not just a prayer.

The Real Cost of Ignoring Risk Control

Before I changed my approach, I made a dangerous mistake: I tried to invest my way out of debt. I read stories of people using home equity loans to buy dividend stocks or putting credit card advances into “sure thing” opportunities. Desperate and misinformed, I considered similar moves. I even opened a margin account with a small brokerage, thinking I could earn returns fast enough to cover my obligations. It didn’t work. The market dipped, my positions lost value, and I ended up with more debt and less confidence.

This experience taught me a hard lesson: risk control isn’t optional, especially when you’re financially vulnerable. When you’re already underwater, taking on additional risk doesn’t accelerate recovery — it increases the chance of total failure. High-risk strategies assume stability, but instability is the condition of debt crisis. Without a safety net, every financial decision becomes a gamble. I realized I needed to protect what little I had before trying to grow it.

The three pillars of risk control became my new foundation: diversification, liquidity, and protection. Diversification doesn’t just mean spreading money across assets — it means having multiple sources of financial strength. That could be a mix of savings accounts, low-volatility funds, and income streams. Liquidity ensures you can access cash when needed without selling under pressure. I learned that having even a small emergency fund changes your decision-making power — you’re no longer forced into bad choices during crises. Protection includes insurance, legal safeguards, and behavioral boundaries, like not using credit for investments. These aren’t glamorous topics, but they’re what keep people from falling deeper when life throws another curveball.

Restructuring Debt with Purpose: A Step-by-Step Reset

Once I committed to a strategic approach, I took concrete steps to restructure my debt. The first was clarity: I listed every obligation — credit cards, personal loans, medical bills — with their balances, interest rates, and minimum payments. I stopped ignoring them and started analyzing them. This wasn’t about shame; it was about strategy. With all the numbers in one place, I could see the full picture and prioritize.

I chose the avalanche method — paying off debts from highest to lowest interest rate — because it saved the most money over time. Some prefer the snowball method, which focuses on smallest balances first for psychological wins. Both can work, but I needed the math on my side. I contacted creditors to negotiate lower rates and extended terms. To my surprise, many were willing to work with me. I explained my situation honestly and asked for hardship programs or temporary relief. Several agreed to reduce interest rates or pause late fees for a few months. This wasn’t forgiveness, but it created breathing room.

I also explored consolidation. I qualified for a personal loan with a lower fixed rate than my credit cards, allowing me to combine multiple payments into one. This simplified my cash flow and reduced the total interest I paid. But I didn’t treat this as a fresh line of credit — I closed the old accounts and committed to not using them again. Consolidation only works if you stop adding to the problem. I set up automatic payments to ensure consistency, knowing that discipline over time matters more than any single decision.

The goal wasn’t just to pay off debt, but to free up cash flow so I could start rebuilding. Every dollar redirected from high-interest payments became a dollar I could use to grow stability. This phase took months, even years, but each payment was a step toward control. I tracked progress monthly, not to obsess, but to stay aligned with my plan. Slowly, the weight began to lift.

Building an Investment Layout That Works in Crisis

Most people think investing is something you do after you’re stable. I learned it’s something you do to become stable. The key is redefining what investing means during recovery. It’s not about doubling your money — it’s about creating systems that grow steadily and survive setbacks. My new investment layout focused on accessibility, consistency, and resilience.

I started small. I opened a low-cost brokerage account and set up automatic transfers of $25 per paycheck into a broad-market index fund. It felt insignificant at first, but I understood the power of compounding. Even small amounts, invested consistently, build over time. I chose index-based exposure because it’s diversified, low-fee, and requires no market timing. I wasn’t trying to beat the market — I was trying to stay in it.

I also created what I called an “emergency-anchored portfolio.” Instead of putting all my available funds into growth assets, I divided them: 70% into stable, liquid accounts like high-yield savings and short-term bonds, 30% into long-term growth vehicles. This structure ensured I could handle surprises without derailing my progress. If an unexpected bill came up, I could cover it without touching my investment stream.

Micro-investing apps helped me stay engaged. They rounded up purchases and invested the spare change. It wasn’t much, but it reinforced the habit. More importantly, it shifted my identity — I was no longer just someone paying bills, but someone building something. The psychological shift was as valuable as the financial one. Over time, those small actions created momentum. I wasn’t rich, but I was moving forward.

Protecting Gains: Why Risk Management Is Your New Safety Net

As my situation improved, I faced a new challenge: protecting what I’d gained. It’s easy to fall back into old patterns when stress fades. I saw friends who paid off debt only to accumulate new balances because they didn’t change their underlying systems. I was determined not to repeat that cycle.

I rebuilt my emergency fund with discipline. I aimed for three to six months of essential expenses, saved in a separate, accessible account. I treated this fund as non-negotiable — only for true emergencies, not vacations or impulse buys. Having this buffer changed my relationship with risk. I no longer feared every unexpected expense. I also reviewed my insurance coverage — health, auto, renter’s — ensuring I wasn’t underprotected. Insurance isn’t an investment return, but it’s a critical part of financial defense.

I practiced behavioral discipline by avoiding lifestyle inflation. When I got a raise or paid off a debt, I didn’t increase my spending. Instead, I redirected that money into savings or investments. This wasn’t about deprivation — it was about intentionality. I allowed myself small rewards, but never at the cost of security. I also set up regular financial check-ins, reviewing my budget, investment performance, and goals quarterly. This kept me aligned and prevented complacency.

Risk management became my new normal. I accepted that slower, safer growth was better than volatile gains that could vanish. I stopped comparing myself to others who seemed to be getting rich quickly. My metric of success wasn’t returns — it was peace of mind. I slept better knowing I had systems in place, not just luck on my side.

The Long Game: From Debt Crisis to Financial Stability

Looking back, the journey wasn’t defined by one big breakthrough, but by thousands of small, consistent choices. There were no windfalls, no miracles, no secret strategies. Just discipline, learning, and a commitment to rebuilding. The debt didn’t disappear overnight, but it lost its power over me. I went from feeling trapped to feeling in control — not because everything was perfect, but because I had a plan that worked.

What I learned is that debt management and investment strategy are not separate goals — they’re two sides of the same coin. Paying off debt is a form of risk reduction, and smart investing is a form of long-term security. Together, they create a financial ecosystem that can withstand shocks. You don’t need to be wealthy to start. You just need to start — with honesty, clarity, and a commitment to structure.

Today, I still follow the same principles: prioritize risk control, invest consistently, protect gains, and think long-term. My portfolio isn’t large by Wall Street standards, but it’s growing. More importantly, I have peace of mind. I no longer lie awake at night. When bills arrive, I open them without fear. That’s the real measure of financial health — not the balance in your account, but the calm in your chest.

If you’re in the same place I was, know this: you’re not alone, and you’re not broken. Your situation doesn’t define your future. With the right mindset and structure, recovery is possible. It won’t be fast, but it will be real. And that’s worth more than any quick fix.